SEC-EDGAR-GPT

A 124M parameter GPT-2 trained on SEC-EDGAR financial filings

Overview

SEC-EDGAR-GPT is a 124-million parameter GPT-2 language model trained on 1.55 billion tokens of SEC-EDGAR corporate filings using the nanoGPT framework. The model was trained on a single NVIDIA RTX 4070 GPU over approximately 8 hours, reaching a final validation loss of 2.28.

We evaluated the model's generation quality across multiple SEC filing sections including business descriptions, management discussion and analysis, risk factors, financial notes, and proxy statements. The model successfully learns SEC document structure, financial vocabulary, and boilerplate language patterns, but exhibits characteristic limitations in long-range coherence, numerical consistency, and table extension.

Training Setup

Model Architecture

| Parameter | Value |

|---|---|

| Number of layers | 12 |

| Attention heads | 12 |

| Embedding dimension | 768 |

| Context length | 1,024 tokens |

| Total parameters | 123.59M |

| Vocabulary | GPT-2 BPE (50,257 tokens) |

Training Data

| Metric | Value |

|---|---|

| Total training tokens | 1.55B |

| Training shards | 16 |

| Validation tokens | 100M |

| Source | SEC-EDGAR via CodeParrot dataset |

| Tokenizer | GPT-2 BPE |

Hyperparameters

| Parameter | Value |

|---|---|

| Effective batch size | 32,768 tokens |

| Learning rate | 6e-4 |

| Min learning rate | 6e-5 |

| Warmup iterations | 2,000 |

| Max iterations | 47,000 |

| Optimizer | AdamW (β₁=0.9, β₂=0.95) |

| Weight decay | 0.1 |

| Gradient clipping | 1.0 |

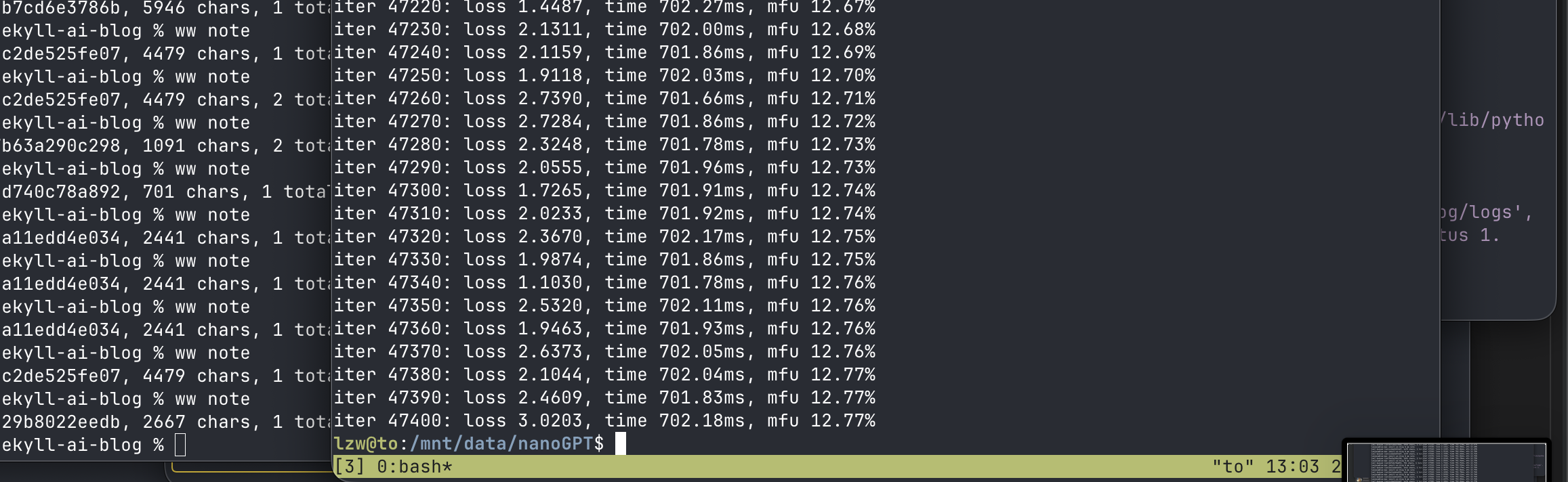

Training Results

Loss Progression

| Step | Train Loss | Val Loss |

|---|---|---|

| 0 | 10.98 | — |

| 1,000 | 3.82 | 3.75 |

| 5,000 | 2.95 | 2.91 |

| 10,000 | 2.62 | 2.58 |

| 20,000 | 2.38 | 2.35 |

| 30,000 | 2.25 | 2.23 |

| 40,000 | 2.15 | 2.22 |

| 47,000 | 2.10 | 2.28 |

Cross-Domain Comparison

| Dataset | Val Loss | Notes |

|---|---|---|

| OpenWebText (GPT-2 baseline) | 2.85 | General web text |

| GitHub Code | 3.466 | Noisy code data |

| SEC-EDGAR (this work) | 2.28 | Clean financial prose |

SEC-EDGAR achieves significantly lower loss than general text and code models, due to the structured, repetitive nature of SEC filings.

Training Completion

Generation Quality Analysis

Five prompts representing different SEC filing sections. Each prompt: 500–2,000 characters of authentic SEC text. Generated 1,000 tokens at temperature 0.7, top-k=100. Evaluation prompts generated with Hermes Agent (Nous Research).

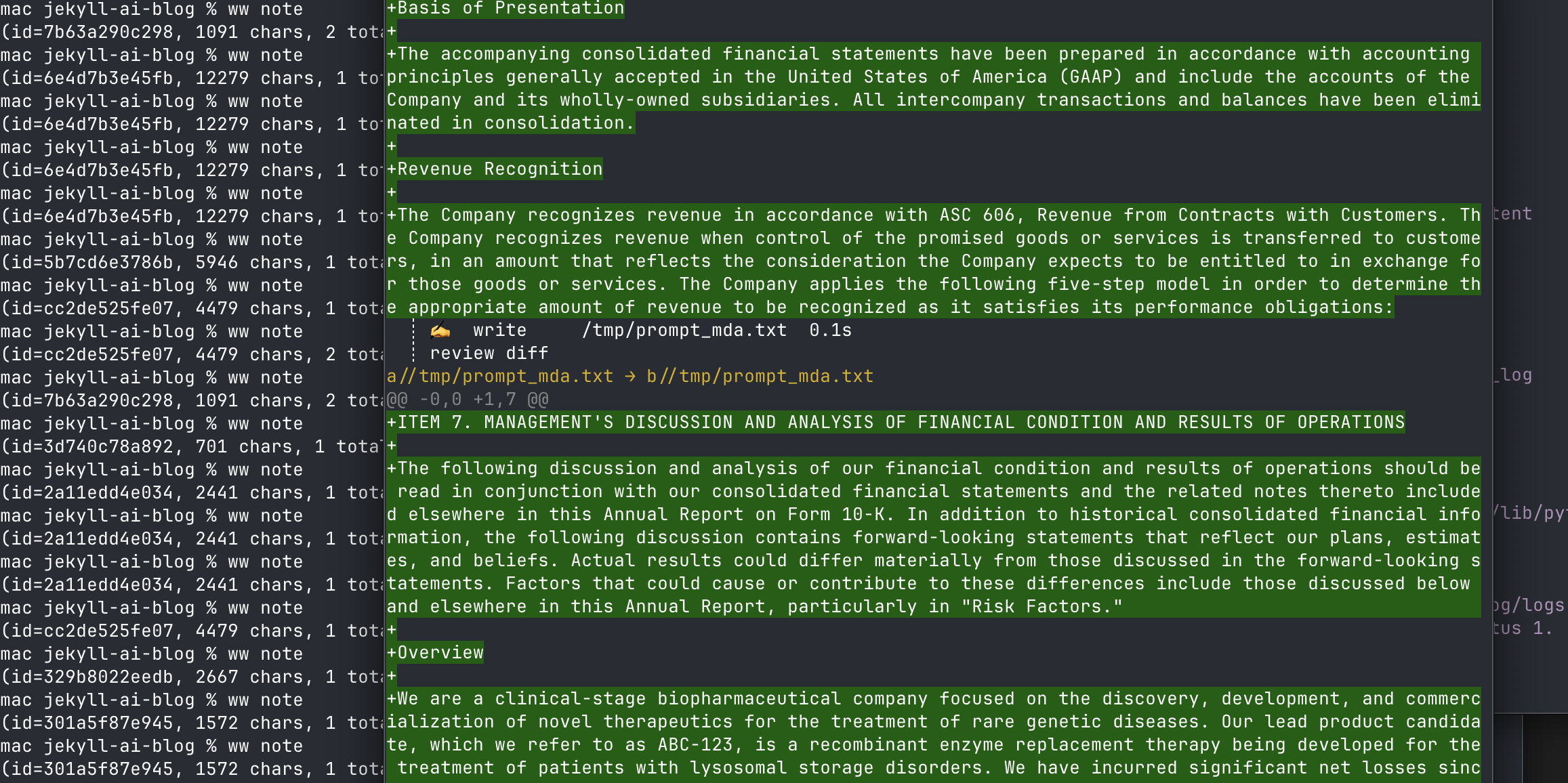

Prompt 1: Business Description (Item 1)

Show full prompt (input text)

Loop "Commercialization of product candidates" repeats 47+ times

Hallucinate Invented drug names: X-Avent, X-Zentib, S-Zentib, Q-partnerib

Prompt 2: MD&A Revenue Analysis

Show full prompt (input text)

Loop 10 consecutive "Cost of revenue increased/decreased" paragraphs

Math Percentages don't match dollar amounts cited

Prompt 3: Risk Factors

Show full prompt (input text)

Loop "Product candidates" appears 47 times in 25 lines

Self-ref Recursive: "product candidates may fail to develop, develop and commercialize"

Key Findings

Echo vs. Generate

The model excels at echoing input content (tables, numbers, formatting) but struggles to generate new content that maintains consistency. It learned surface-level patterns rather than underlying data relationships.

Loop Attractors

Certain phrases act as "probability sinks" when the model is uncertain:

"Commercialization of product candidates"— biotech 10-K risk factors"Cost of revenue increased by $X million"— standard MD&A opener"Raise additional capital"— going-concern disclosures

Numerical Coherence

- Dollar amounts: Plausible scale ($1M–$500M) but internally inconsistent

- Percentages: Often don't match the dollar changes cited

- Dates: Consistent (always "December 31, 2023/2022")

- Implication: The model learned the format of numbers, not their meaning

What It Can Do

- Generate SEC boilerplate language and standard disclosures

- Suggest section structures and formatting conventions

- Draft placeholder text that visually resembles authentic filings

- Provide a starting point for human writers to edit and refine

What It Cannot Do

- Generate accurate financial data or calculations

- Maintain consistency across long documents

- Produce factually grounded content

- Extend tables with new, coherent rows

Citation

@misc{sec-edgar-gpt-124m,

author = {Zhiwei Li},

title = {SEC-EDGAR GPT-2 124M},

year = {2026},

publisher = {GitHub},

url = {https://github.com/lzwjava/sec-edgar-gpt}

}